The 2025 / 2026 tax year begins on 6th April and the stocks and shares ISA allowance will stay the same for the 9th year running. So that’s an overall tax-free investment limit of £20,000 per adult. Junior ISAs for under 18s have a separate £9,000 allowance.

Although cash ISAs are the most popular and straight forward option, you should really consider a stocks and shares ISA when investing for the longer term. By that, think 5 years and beyond.

Also known as ‘Investment ISAs’, these are tax free accounts to place your money into not just shares, but government and corporate bonds, property and a choice of thousands of different investment funds.

Investing in the stock market brings volatility risk into your life, so the value of your savings will move down as well as up on a day-to-day basis. But over the longer term, your money has a better chance of increasing its spending power.

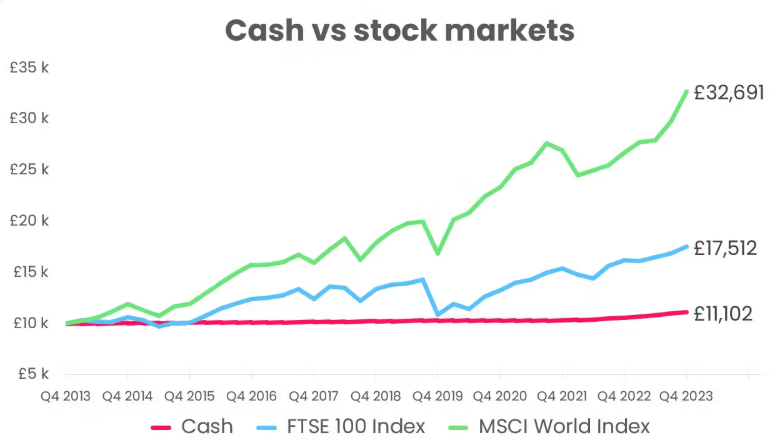

The graph below from education and comparison site Boring Money gives an idea of how the growth of £10,000 in cash has compared with the growth of the FTSE100 and the MCSI World Index over a 10 year period.

Growth of £1,000 over 10 years: cash v shares

Growth of £1,000 over 10 years: cash v shares

Note that share values move up and down all the time and chances are that over the short term, investments will drop below their original value. But the declines have always proven to be temporary, whilst the long-term advance has been permanent.

1. Expect volatility and learn from the experience

Many people are put off from investing into stocks and shares due to the risks involved. That’s understandable and it’s true what all the warnings say. The value of your investments can fall as well as rise and past performance is no guide to the future.

Over the years, I’ve spoken with many people who have lost out on investments. It nearly always comes down to a lack of diversification (owning shares in only a few or even just one company) or a behavioural reaction. For example, panic selling when the markets are down.

This largely stems from a lack of knowledge, experience and understanding. That’s not a criticism, by the way, and it’s not about being “stupid”. We don’t learn about this at school, so we can hardly be blamed for lacking in confidence when it comes to money management and investing.

The good news is that it doesn’t have to be complicated or difficult. It’s now easier than ever to begin building wealth without having to choose individual companies to invest in. There are plenty of modern and accessible investment providers, ranging from self-select DIY platforms to automated advice or “robo-advice”, right through to comprehensive, personalised advice.

For more about investing for the first time, read my article “5 easy and empowering steps to make your first investment“.

2. Choose your stocks and shares ISA pathway

It can be hard to know where to begin, but comparison sites are a good start. They let you see the main providers with details of their charges, investment options and customer service standards.

There’s the well-known MoneySavingExpert.com which outlines 2 approaches, depending on how confident you feel:

- Do-it-yourself: self-research “DIY” platforms

- Do-it-for-me: automated “robo-advice” platforms

There’s also the well-established Which? with a host of information and easy-to-follow guidance.

Boring Money offers a list of ‘best buy’ ISAs for 2025, as scored by customers.

It’s more than likely that your own bank will also offer access to stocks and shares ISAs, but it’s worth understanding the charges and levels of service before going ahead.

You can also seek guidance and support from a financial coach or a financial adviser. Read more about the differences between financial coaching, planning and advice here.

3. Compare the costs

Charges for stocks and shares ISAs can be a bit confusing at first. You can expect a ‘platform’ charge, which covers administration costs for the provider. On top of this, there will be a fund management fee to cover the actual investment costs of the underlying funds.

For example, Moneybox charges a platform fee of 0.45% of your investment value per year, plus £1 per month. For this, you get a user friendly app for mobile devices and you can link it to your bank account to round-up your transactions to the nearest pound and invest the difference.

In addition to the platform fee, you would pay investment fund charges of between 0.12% and 0.58%. So overall, you would expect to pay between 0.57% and 1.03% plus £1 per month for a Moneybox ISA. It doesn’t sound much, but over the years, it will have the effect of slowing down the growth of your money.

Vanguard is known as one of the cheapest investment providers. For example, their platform charge is only 0.15% and fund management charges for their LifeStrategy range are 0.22%. But it’s not quite as user friendly for mobile device users.

Wealthify is another investment app with a platform charge of 0.6% plus average fund management charges of 0.16 for ‘Original’ and 0.7% for ‘Ethical’ funds. This provider offers “robo-advice” to help you select the most appropriate funds.

4. Understand the risks

ISA providers offer a choice of funds to suit your risk level, from cautious (lower risk) through balanced (medium risk) to more adventurous options.

What this really means is the extent to which you can expect your investment to fluctuate in value. The more you invest in equities (shares) the more you can expect day to day movements, compared to investing in bonds or cash.

Investment portfolios often include bonds to help balance out the volatility of shares. Bonds are loans to companies and governments and whilst they also fluctuate in value, they are generally more stable.

Despite the short-term volatility of stocks and shares, it’s worth remembering that relatively ‘safe’ Cash ISAs are not without risks of their own. Over the long term, cash will struggle to keep pace with rising prices. So the spending power of your savings can be eroded over time – this is inflation risk.

In short, there is no ‘risk-free’ option at all, so don’t let investment volatility put you off when it comes to long term planning.

If all of this feels like information overload and you don’t much fancy doing all the research, then financial coaching or regulated financial advice might be a way to cut through to a quicker decision.

5. Watch out for stocks & shares ISA restrictions

The annual allowance of £20,000 will be more than enough for most people, but remember, if you don’t use this allowance, you lose it. The annual limit includes payments into cash, stocks & shares, lifetime and innovative finance ISAs.

You can only pay into one of each ISA type per tax year. So although you can own more than one Stocks and Shares ISA, you can’t pay money into more than one during each tax year (6th April to 5th April).

Withdrawals from ISAs are usually easy enough, but take care with investment ISAs. Only invest if you plan to leave the money to build up over several years. You wouldn’t want to be forced into withdrawing money, just at the point where markets take a dip.

Summary

More and more responsibility is being placed on us, as individuals, to plan for our financial future. Final salary pensions are disappearing, and the state pension is creeping further away from us as the qualifying age increases from 65 to 67 by 2028.

ISAs can be a great way to invest for financial options later in life, with no tax on the growth and no tax when you withdraw money later down the line.

The only problem is, not enough of us are investing for the future. Why not challenge yourself to make better use of your tax-free ISA allowances?

For more information about the range of different ISAs, click here.

Production

Production