The days when my bank colleagues and I manually assessed credit applications and made personal and business lending decisions are long gone. It’s nearly all based on automation now, which is why it’s so important to boost your credit score.

Building and maintaining a high credit score will help secure the best deals on credit cards, loans, mortgages and more. It can affect eligibility for the best mobile phone contracts, utility bills and even rent applications.

It’s easy to dismiss debt as a ‘bad’ thing, but none of these products are bad in themselves. It’s financial behaviours and spending patterns that tend to cause most problems with money. So, if you want to savour your spending and be in control of your daily finances, let’s delve into the mysterious world of credit scores.

What makes up a credit score?

First of all, it’s useful to understand that lenders will use one or more credit reference agencies to help assess whether or not you are ‘good’ for credit.

We’ll look at the 3 main credit reference agencies in the next section, but they all use a scoring methodology provided by the Fair Isaac Corporation, or FICO. This is a data analytics company based in the US and was founded in 1956 by Bill Fair and Earl Isaac.

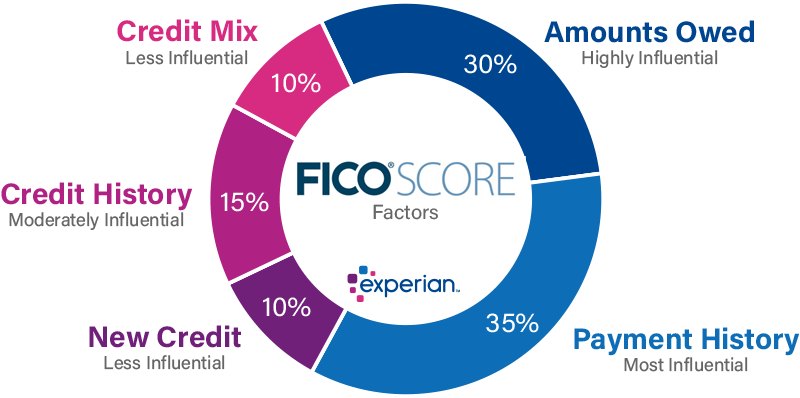

As you can see from the image, there are 5 key components that make up your credit score:

1. Payment history

This is the most important element of your credit score and reflects how well you’ve kept up with payments in the past. Missed or late payments to loans, mortgages and credit cards etc will have a negative impact.

2. Amounts owed

This is a measurement of the proportion of available debt that you are currently using. It’s the 2nd most important part of your overall credit score and can indicate how reliant you are on credit. If you’re using more than 30% of your available credit, this can have a negative impact.

3. Length of credit history

This takes account of how long you’ve held credit. Not just your oldest credit account, but also your newest and the average age of all credit agreements. The longer your credit history, the higher your score, generally speaking. This only accounts for 15% of your overall score, though.

4. Credit mix

This recognises the variety of debt that you’ve used in the past. For example, a range of car loans, credit cards, mortgages, phone contracts and so on. It helps indicate how well you manage a range of different credit products.

5. New credit

This element is affected if you make a lot of credit applications in a short space of time. It could indicate an increased credit risk and potentially have a negative impact.

What’s a good credit score?

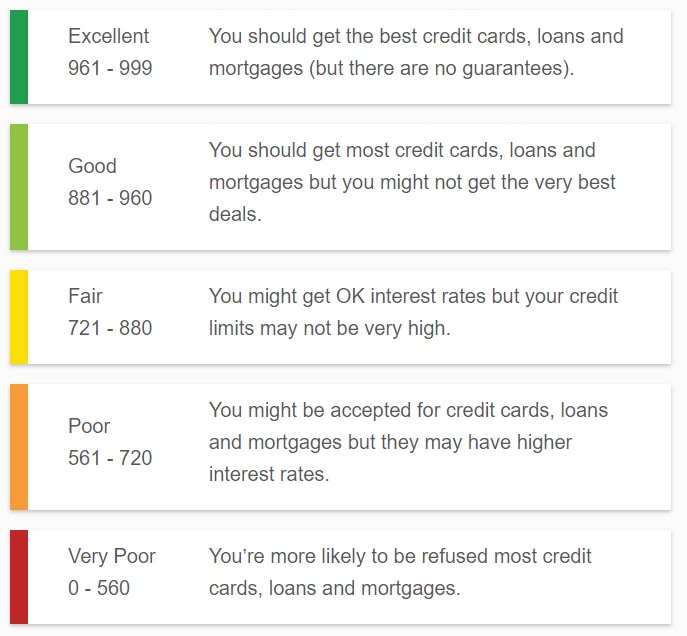

Your credit score is a 3-digit number, where higher is better. What makes it all a bit confusing, is that different credit reference agencies use different criteria and scoring models.

But generally speaking, they all describe your creditworthiness in 5 levels. To use Experian as an example:

According to Experian, the average credit score is 797, described as ‘fair’. As you can see from the table, to boost your credit score is to improve your chances of qualifying for the best credit cards, loans and mortgages.

What are the main credit reference agencies?

There are a growing number of credit reference agencies, or “bureaus” across the globe, but let’s take a look at the top 3.

You can register with one or more of these to access your credit files for free, although charges may apply after an initial trial period.

Experian describes itself as “the leading global information services company”. The California based organisation operates in 37 countries with corporate headquarters in Dublin and operational headquarters in Nottingham, UK and in Brazil.

Equifax claims to be the market leader in most of the 24 countries in which it operates. It’s based in Atlanta and is especially dominant in the South and Midwest of the USA.

TransUnion is Chicago based, with regional offices in the UK, Hong Kong, India, Canada, South Africa, Colombia and Brazil. It markets itself as “a global information and insights company that makes trust possible”.

Lenders will generally use information from one or more of the above bureaus when processing your credit applications. That’s why it’s important to make sure the information they store about you is correct, then you can take steps to boost your credit score.

What about your ‘affordability score’?

A relatively new part of your overall credit file uses Open Banking to estimate future ability to repay debt. This collates up-to-date information from your bank accounts, including current income and expenditure. That’s different to your credit score, which is based on historical information.

To find out your affordability score, you need to link your bank accounts to an account like the moneysupermarket.com Credit Club. This operates in partnership with TransUnion and is an excellent resource of free information, hints and tips.

You can also sign up for other free services to manage your credit file, including ClearScore for Equifax and CreditKarma for TransUnion.

The combination of your credit score and your affordability score will give a good indication of how likely you are to be accepted for the best credit offers. Note that it’s possible to have a high score in one, but a low score in the other.

Having a perfect credit score doesn’t guarantee that you’ll be accepted for a loan or mortgage. Lenders want to check that you have sufficient disposable income to afford monthly repayments. It’s not all about your credit history.

The advantages of an excellent credit score

Perhaps the most obvious advantage in having a high credit score is your improved chances of getting a mortgage or loan approved. There are less obvious benefits too, so it can be valuable to boost your credit score, even if you don’t plan to have ‘debt’ in the traditional sense.

Pay less interest

An excellent credit score translates to less risk for the lender. As such, you’re more likely to benefit from lower interest rates on credit cards and loans.

Better mobile phone contracts

When locking into a contract that includes the latest mobile device, that will involve a credit agreement. When mobile phone providers run a credit check, they could decline applicants with a low credit score. This means you could end up with an inferior deal or a pay as you go contract instead.

Easier renting

Landlords and letting agencies will often run a credit check on prospective tenants. A poor credit history could result in losing out on a property, or perhaps having to provide a guarantor.

Cheaper car insurance

If you pay by instalments, your insurance provider will check your credit score and this could affect the pricing of your monthly premium. Statistically, it seems that people with low credit rating are more likely to make car insurance claims, so this can feed into pricing. You can read more in this article by CompareTheMarket.

More employment options

This won’t be true for everyone, but careers in areas like law and finance often involve a credit check as part of the recruitment process. A poor credit score could potentially stall career prospects in some cases.

How to boost your credit score

Even if you don’t have plans to “get into debt”, it can still pay to maintain and boost your credit score.

One of the basics is to ensure you are on the UK electoral role with an up-to-date address. This provides proof of address to credit reference agencies, so make sure that you have registered to vote.

You might expect all of the information on your credit file to be correct, but mistakes do happen.

Check the accuracy of your credit file once a year or so, and make sure all your information is up to date. Even a mistyped address can negatively impact your credit score.

Build your credit history by making payments on time. This includes loan payments, utility bills, mobile phone payments, insurances etc. Make sure you have direct debits to automatically pay bills on time and organise bank accounts in such a way that funds are always available.

Keep your credit utilisation low. This means try to maintain debt levels well below what you have available to borrow. This helps to show lenders that you can manage money effectively. Try to repay the full balance on credit cards each month and think carefully before cancelling old credit cards. Reducing your overall credit limit will increase the percentage that you do use and this could potentially lower your score.

Perhaps a slightly more drastic way to improve your score is to end your financial association with other people who have a low credit score. This could be tricky when you have joint bank accounts with a partner, but if they have a poor credit history, it could affect your own credit rating. Removing that link could boost your score within a month.

Summary

There’s more to having an excellent credit score than just having better access to debt. In today’s world, it’s important to begin building evidence of financial responsibility from a young age. That means being able to handle payment contracts, loans and credit cards without getting into trouble.

We all have money challenges, though. Unexpected expenses, financial emergencies and poor spending choices can all result in debt building up to a point where it feels uncomfortable, or worse.

Knowing how to boost your credit score can give you an advantage in many aspects of financial life, but even if you feel ‘over your head’ in debt, there’s nearly always a way out. You can read more about how to eliminate your debt here and if you’d like to talk about this, why not arrange a free initial chat to find out if financial coaching could help?

Don’t forget, you can also get free help and advice from a range of debt charities, for example, the excellent Step Change.

Production

Production