When your monthly income hits your bank account, do you pay yourself first, ahead of all the other bills? Most people don’t, yet it’s one of the easiest and most effective ways to build wealth for the future.

Think about your future self and the lifestyle you’d like to enjoy later down the line. Assuming you want to enjoy a degree of financial freedom, whatever that means to you, it’s vital that you make a conscious decision to invest in your future self. That means balancing what you spend now against what you want to have in the future.

One of the most effective strategies for building up financial security is to prioritise automatic, regular savings before anything else. Before your mortgage or rent, your bills, your groceries, leisure spending and everything else. You need to pay yourself first.

Unfortunately, most people do the opposite. The usual approach is to receive your salary, pay all the bills, holidays and socialising and then see what’s left at the end of the month. It just doesn’t work.

If you value yourself and your future financial security, this is the wrong way round. You need to flip the approach and adopt “reverse budgeting”.

4 reasons to pay yourself first

1. This is a behaviour that says “I matter”

You prioritise your long-term financial wellbeing and create more of a balance against the relentless bombardment of spending temptations that come along each day.

2. It builds financial confidence

As you see the value of savings and investments grow over time, confidence will grow. Because it becomes habitual, you don’t even miss your regular savings contributions after a while.

3. Financial discipline becomes one of your strengths

Over time, you’ll find ways to cut back on unnecessary expenditure and boost the amount you save.

4. Wealth doesn’t just happen

You need intention, action and time. That doesn’t mean it’s difficult. You just need to follow some easy steps to make it happen and stick with it.

5 steps to begin paying yourself first

1. Decide an amount to begin with

Don’t worry too much about what the right amount is. Just start by creating the habit. £25, £100, £500 per month…..whatever you feel is manageable. In fact, even better is to start saving an amount that feels slightly uncomfortable.

2. Automate your savings

Set up a standing order so that money comes out of your salary account immediately after payday. It should go into a separate savings or investment account that you can’t dip into so easily. If you have a Save As You Earn scheme available at work, that could be a good option. Or some modern digital banks like Monzo and Starling allow you to set up separate ‘pots’ without needing separate accounts.

3. Increase your savings periodically

As you get used to making the payments, challenge yourself to increase your standing order every so often. Especially if you get a pay rise or if any of your other bills decrease.

4. Don’t break the habit

Make sure you pay this ‘bill’ every pay day without fail. Don’t be tempted to dip in to the savings except for genuine emergencies. This is a long-term investment in yourself, so treat it with the same importance as your mortgage or rent.

5. Start now

Don’t wait for your next pay rise. Avoid having “just one last month” of spending freely. Don’t wait until you’ve worked out the perfect amount to save. Do it now, however small, just set up that standing order to start the habit.

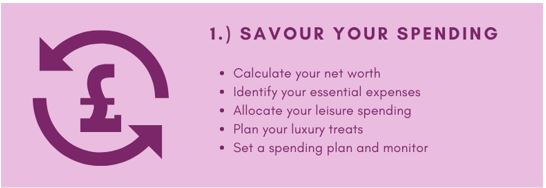

Savour Your Spending

It can help to become more intentional and aware of how you spend your money and your time. What gets measured gets improved, so every so often, calculate your net worth and create a spending plan that enables net worth to grow.

Read more about how to savour your spending here.

What if you have debts?

If you are paying off mortgages, car loans, credits cards etc, the same principle can help reduce those debts more quickly. Arrange over-payments straight after pay day and consider allocating even a small amount towards savings. This can help build up an emergency fund, which could help you avoid taking out more debt in the future.

If you’re considering taking on new debt, possibly to fund a new car or house purchase, set aside a ‘Pay Yourself First’ amount before deciding what’s affordable to borrow. This might mean lowering your expectations on the next big purchase, but it comes back to creating that balance between spending now and your future financial wellbeing.

Summary

‘Pay Yourself First’ is one of the golden rules to building wealth. It’s more about developing a financial behaviour than anything else, so to begin with, you don’t need to worry too much about how much to save or where to put your money.

In time, you can explore more about the financial products available, such as ISAs, pensions and others. And once you get used to your automated payment, you’ll become confident to increase the amount you save.

So, just make a start. Open up a separate savings account, if you don’t have one already. Set up a standing order with your bank. Then sit back and let your money and automatic payments do the work.

Often, a feeling of overwhelm, competing priorities and procrastination prevents action. Financial coaching can help you gather your thoughts, prioritise, and keep motivated. Breaking it all down into small, step by step actions will get the results you want.

Production

Production